When national governments run mobile broadband networks, they do not run them well. That’s the unsurprising conclusion of a white paper published by GSMA, the trade association for mobile network operators that rely on GSM standards to one extent or the other – in other words, pretty much all of them.

A trade association that lobbies governments to advance the interests of its members might be expected to oppose what amounts to nationalisation of mobile network infrastructure and operations. So it’s hardly shocking that GSMA’s brief overview of publicly-owned open access mobile networks – the government or a favored company builds one, single network and sells wholesale space on it to mobile retailers – doesn’t have much good to say.

But the report should be judged on its merits, and not dismissed simply because of the source. On that basis, it does point to a couple of supportable, and pedestrian, conclusions.

First, it highlights an ordinary truth about big government infrastructure projects: far more are proposed than implemented, and even the ones that move forward usually aren’t started, let alone completed, on schedule. The paper looks at five open access mobile network initiatives. Three – in Kenya, Russia and South Africa – never began, and one, in Mexico, is taking shape slowly, with no guarantee that anything will actually be built. In that sense, mobile networks are little different than other government led infrastructure projects.

Then there’s the fifth network, in Rwanda. It was actually built, in a public-private partnership with KT, a big South Korean telecoms company, and it’s been operating for about three years. Build out has been slower than planned and might never reach its target of covering 95% of the population, but it does reach something like a third of the population and it’s the only source of 4G LTE service in the country.

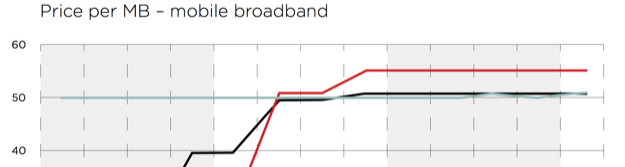

The GSMA white paper is woefully short on details, but it does provide one interesting, quantitative indicator that few benefits have flowed to consumers, at least not yet. Since the open access 4G network was launched late in 2014, the price of mobile broadband service has stayed flat – the three major mobile operators all charge around 6 cents per megabyte/$60 per gigabyte.

That’s also not surprising. To the extent the three companies re-sell service on the Rwandan open access 4G network, they all have the same wholesale cost. With only three players, the mobile market is very concentrated, which means it’s less likely that they’ll engage in a profit-killing, price led race to the bottom.