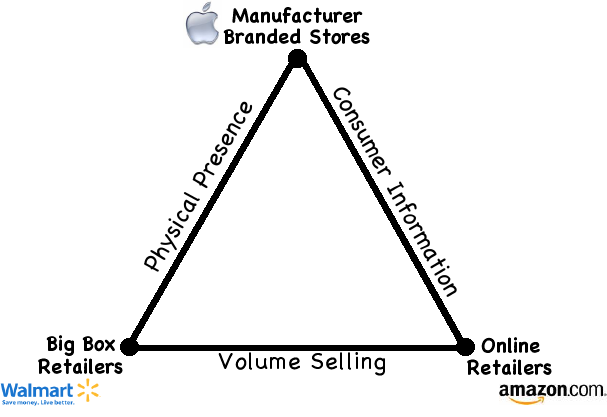

21st Century retailing will be governed by a new Iron Triangle:

- Consumer information.

- Volume selling.

- Physical presence.

Online retailers have inexhaustible information and limitless volume. Consumers save time and money.

Big box retailers have as much volume, and a physical presence that allows consumers to touch and feel products however they choose, and have the instant gratification of an on-the-spot purchase. Customers stay in control.

Manufacturers can sit back and enjoy the ride, or they can build the value of their brands by combining their ultimate control of information with a physical and/or virtual presence that promotes a direct personal relationship with consumers.

CES and MacWorld have sprung leaks, with attendance expected to be down. MacWorld’s survival is in doubt. CES will ride out the storm, but even old salts are looking green around the gills.

The two shows suffer from exactly opposite problems. MacWorld is the victim of Apple’s retail success, while CES is being battered by the failures of consumer electronics retailers. Circuit City’s financial meltdown and Best Buy’s preemptive self-cauterization are just the beginning of what will be, for many, a wrenching disruption of the consumer electronics retailing model.

The major CE chains are headed for extinction, killed by the same trends that created them. In the 1980’s, televisions, VCRs, and audio gear became more reliable, easier to use and increasingly compliant with nascent industry standards. The need for hands-on sales, support and service expertise fell. At the same time, logistics and inventory management were transformed from back office, seat-of-the-pants jobs into scientific disciplines with seats on the board.

The less expertise required of sales and other customer-contact personnel, the less the salaries. A small team of number crunchers, transportation specialists and information technologists could run national chains of CE superstores. It didn’t matter how much money they made. In fact, the more they were paid, the farther superstore chains pulled ahead.

With size came the ability to take advantage of ever growing brand building tools. Customers might not have known exactly what they wanted, but they knew where to find it.

The superstores, however, carried the seeds of their own destruction. In a shipping container and a computer, an SKU is just an SKU. From the forklift operator on the loading dock to the clerk at the checkout register, boxes flowed through CE stores in an ever growing torrent.

The problem, for superstores, was that once the expertise required of the customer contact personnel dropped below a second threshold, it didn’t matter what was in the boxes. It could be a television or a washing machine. Or disposable diapers, or children’s clothes, or potato chips. At the same time, there was explosion upon explosion in the information available to consumers. Increasingly, consumers knew what they wanted before they ever set foot in a store.

Now, the not-so-super CE stores look like 98-pound weaklings next to the real big box retailers. The big box guys took even better advantage of the same trends and technologies that fueled the growth of CE superstores.

But they aren’t the only ones who successfully rode these giant waves. Manufacturers did too, taking ruthless advantage of new communications technology and advertising media to leap over distributors and retailers, and establish direct relationships with their millions – billions – of customers. The more that manufacturers spoke directly with consumers, the less they needed retailers. Except to drive forklifts and ring up sales.

For that, you don’t even need a bricks and mortar retailer. The Internet changed the game. If you’re Consumer X, and you have a personal relationship with Manufacturer A(pple), it’s a lot easier to go online, google “iStuff” and click on the lowest price.

If you don’t know what you want yet, you go to the A(pple) store if one is nearby, and look at the iStuff and talk to sales people in black shirts who have actually had a day and a half of training. If that’s not enough, you can have an audience at the geek altar, I mean, a conversation at the G(enius) B(ar).

CE superstores tried to optimize volume, information and physical presence, and did so successfully for a while. But only a while. Bigger players who are maximizing their advantages in just two ruling factors are circled around those erstwhile optimizers, and are rapidly crushing them. There’s no telling how long this new Iron Triangle will rule consumer electronics retailing – the world is not done changing – but it’s clearly in command now.